This blog follows the real-life story of Antti (name changed for privacy) as he started his stock trading journey and needed to figure out how to do related tax matters.

Disclaimer: This article only discusses the Finnish taxes associated with selling shares, not taxes imposed under other tax jurisdictions. This is also not a replacement for advice from an accountant or personal finance advisor.

—

The year is 2020. February. As Antti’s colleagues enthusiastically talked about the rise of Tesla (TSLA) stock at the time, Antti made the decision to “jump in”. It’s time to start investing. He has some savings outside of his emergency funds, so why not let the money work for him?

His only concern is tax. Being a young professional, he just recently got used to the concept of a tax card. And even that still kind of makes him nervous.

Trading platform

Antti’s first step is to figure out what trading platform to use. There are quite a few. And from the perspective of tax-paying, there are two types of platforms, one that automatically report Antti’s tax responsibilities to the tax office (Vero), and one that does not. In the latter platforms, Antti will need to report it to the tax office himself for every selling transaction that he makes.

If Antti really doesn’t want to deal with the hassle of reporting tax, he should start buying stocks from bank apps like OP, Nordea, Danske Bank, or Nordnet, which is a popular choice for stock investments in Finland. These platforms automatically handle the tax reporting.

Antti also has a bunch of other trading platforms to consider, like eToro, Degiro, plus500, or Coinbase if he wants to buy some cryptocurrency or commodities. These are internationally known platforms and boast about low-commissions, no hidden fees, etc… However, if Antti decides to use these apps, he will have to declare tax on capital gains (or loss) himself.

Capital gains tax also includes the realized gains from bonds, real estate, property and precious metals; and it is different from personal income tax, which is typically from your salary.

Buying shares

There is a way for Antti to put off taxation for a long long time until he has grown wiser. That is, to buy and hold the stocks. However, he should probably not buy a stock as volatile as TSLA, unless he really believes that it will go to the moon and stay there (which it did, in 2021, so far).

However, Antti had a bit of an unhealthy obsession over Elon Musk, so bought TSLA, he did. Now Antti is a certified investor.

You probably noticed that TSLA is listed on NASDAQ, which is US-based. However, when it comes to stocks nationally in Finland or globally, the rules to taxation usually apply similarly. This is also true for listed and non-listed companies. We will discuss this below.

Selling shares

One week later, TSLA soared from 600€ to 700€. Antti thought it had peaked, so he is thinking of selling it now to cash in.

Minimum annual taxable amount

First thing to note, is to note how much Antti sold his TSLA shares for. According to Vero, if the annual amount is less than 1,000€, then there wouldn’t be any taxation. However, Antti is selling 10 shares at the price of 700€, which is 7,000€ worth* in total. So there will be taxation.

*Please note that this 1,000€ refers to the revenue gained by selling shares, not the profit.

Capital gains tax calculation methods

Capital gains tax is calculated from capital gains, which equals Revenue – Cost. And there are two ways to determine cost, 1) is through the purchase price + expenses incurred in making a profit or 2) the deemed acquisition cost.

Purchase price + expenses

The first way is quite simple and just like the name. The expenses incurred could be the brokerage fees that Antti pays to the trading platform, say 5€. Antti purchased 10 TSLA shares at 600€, so total purchase price was 6,000€. At the fees on top, it is 6,005€. His profit would be 7,000€ – 6,005€ = 995€. The tax will then be derived from Antti’s profit, the 995€.

Deemed acquisition cost

The second way is a bit more complicated, because it depends on the holding period, i.e. how long Antti kept the shares for. If Antti held the TSLA stocks for over 10 years, the deemed acquisition cost is 40% of the selling price of the shares. If the holding period is less than or equal to 10 years, the deemed acquisition cost would be 20%.

But how to incorporate this “deemed acquisition cost”? The amount that is taxed would be Selling Price – Deemed Acquisition Cost. In other words, whatever’s left after minusing out the deemed acquisition cost. So in the case of Antti, if he chooses this way of calculating tax, it will be as follow:

Since he has only held the TSLA stocks for a week, his deemed acquisition cost is 20%, he will be taxed for the other 80%, which would be 7000€ * 80% = 5,600€.

Choosing which way to declare tax

Assuming the objective here is to gain as much money as possible, Antti would want to pay as little tax as possible. In this case, Antti should go with the first way of calculating through purchase price and expenses. 30% tax on 995€ would be a lot less than 30% on 5,600€. He would even make a loss in the latter scenario.

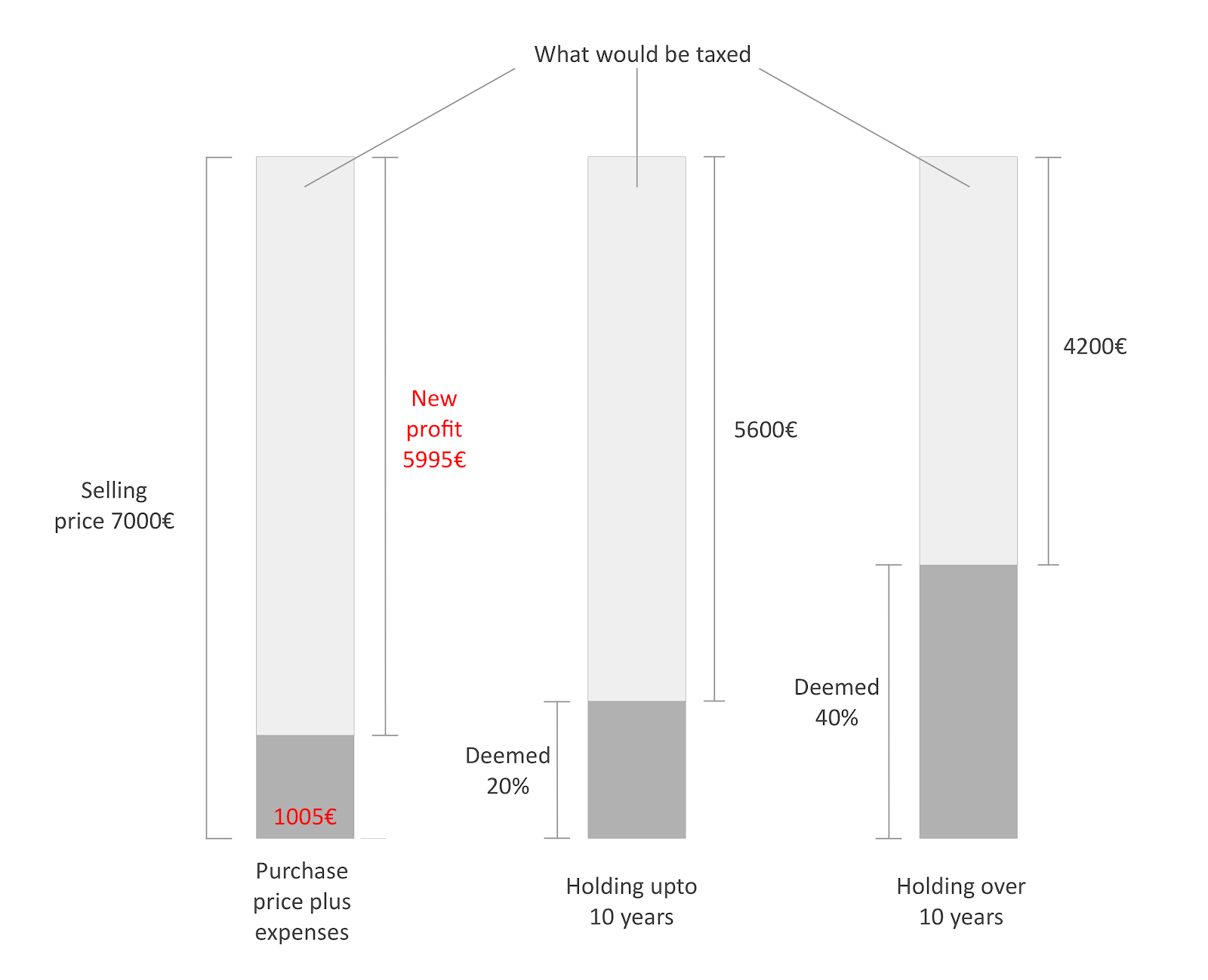

So why would one ever want to get taxed through deemed acquisition cost? Good question. Here is an illustration that will aid our understanding.

Figure 1. Antti’s options for declaring tax

Drawing this out made Antti wonder, even if he held the stocks for over 10 years, the 40% deemed acquisition cost would still be worse than basing off of purchase price + expenses. Well, yes and no. It is true if the stock price would be 700€ per share at that point in the future, which is highly unlikely.

Antti realizes that deemed acquisition cost would only be beneficial when the profits are incredibly high, like moon high. In other words, the selling price needs to somehow climb up to the point where the purchase + expenses % would be lower than the deemed acquisition cost %.

If Antti could go back one year in time and buy TSLA when it was at 100€ per share, even 20% deemed acquisition cost would be much better than purchase price + expenses. The illustration would be like this.

Figure 2. Antti’s options for declaring tax at new purchase price

In practice, it is very difficult to predict a stock with such exponential growth, so typically taxation with purchase price + expenses is the way to go.

Tax on capital gains

Now that Antti has decided the method of calculating the amount to be taxed, he wants to know how much the tax amount is. When you sell shares at a profit, you pay according to the capital gains tax rate. Up to 30,000€, the tax is 30%. Over 30,000€, the tax is 34%. If this TSLA shares selling is the only sales transaction Antti makes this year, he would be paying 30% of the 995€ profit to tax, which is 995€ * 30% = 298.5€.

Conclusion

A year has passed since Antti bought and sold TSLA shares. He made some money, but also lost out on a lot since TSLA rocketed. But that’s life, Antti has moved on. At least now he is wiser and no longer worries about tax-related matters. He can focus on learning how to invest properly, instead of jumping on hypes, as he probably should’ve done in the beginning.